Anyone who follows this blog knows I am a big fan of real estate, especially direct holdings of residential rental properties.

This world is constantly changing.

But no matter how much the world changes, I can’t see people not finding a place to call home. We will always need a roof over our heads, a kitchen to prepare food, bathrooms for personal sanitation, and bedrooms for sleeping. In other words, I can’t see residential real estate being disrupted by technology or going out of favor.

There are also many advantages to owning real estate from having the ability to acquire a real estate property for below market price, to the usage of leverage, to the wonderful tax advantages of real estate. Those tax advantages allow me to cash flow a six-figure amount without paying any income taxes. How great is that?!

Those are just some of the benefits of owning residential rental properties. There are a few more. It is no wonder I think real estate should be the cornerstone of everyone’s investment portfolio.

This has been a love affair 15 years in the making when I first got a taste of what being a landlord is like by buying an owner occupied duplex. I lived in one unit and rented out the 2nd unit. Since then, I knew I wanted to grow my real estate portfolio.

There are 9 reasons why I think buying an owner occupied property is a good first step into rental properties. I continued to add to my rental property portfolio over the ensuing years.

I currently own over 20 rental units with the majority located in New York City.

Real Estate Is Quite Attractive In Today’s Environment

In my opinion, today’s environment makes real estate quite attractive.

The U.S. Federal Reserve is injecting the U.S. economy with trillions of dollars to combat the economic recession exacerbated by the global pandemic. It is hard not to see real assets going up in value after the economy starts on its path to recovery given there are trillions more dollars in the hands of people.

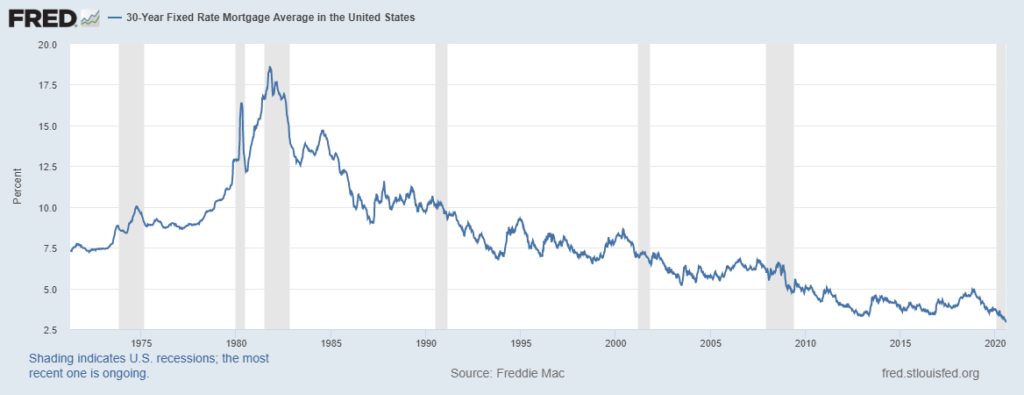

We are also living in a very low interest rate environment. The same goes for mortgage rates. The 30 year fixed rate mortgage has never been lower in history. Borrowing is extremely cheap.

What do you get when you combine assets that can benefit greatly with the trillions of dollars printed by the Fed and a very low cost of financing to acquire those assets? I call this a recipe for financial success.

Acquiring real estate with cheap financing is also how I end up achieving a 10% cash on cash return on my capital and 18% total return.

Even with all those great benefits and macro environment working for residential real estate, this is the first time I’ve thought about not adding to my investment portfolio going forward.

“What gives?” you might think. Is my love affair with real estate over?

I don’t believe my love affair is over with real estate, but it has certainly dimmed quite a bit.

My current situation is unique to my own investment portfolio and personal preferences. But I have the following 8 reasons why I am going to think long and hard before adding to my rental portfolio.

The 8 Reasons Why I Am More Hesitant Than Ever To Add To My Rental Portfolio

Reason #1: The More Rentals, The More Headaches

Rentals are work. Anyone who tells you otherwise isn’t giving you the whole truth. The more rentals, the more work.

There are many issues and headaches that pop up in having 20 plus rentals.

Here is a sampling of some of the more recent issues I have to deal with across my properties over the past couple of weeks:

A Jacuzzi tub I have in one of my rental units went on the fritz. The motor started running even though the renter had no interest in using the tub. He didn’t know how to close it and I had to connect with a few previous tenants to ask them since I am not familiar with the working of the Jacuzzi. Nonetheless, the on/off button wasn’t working and I had to get a contractor in there to fix the problem. All told, it took numerous calls and text messages to get the issue resolved. This happened when I was out taking a nice hike with the family.

I had to order a dishwasher lower spray arm for another renter because the original one melted due to the heat of the hot water. This entailed researching the part to order, ordering it, and then sending my renter a video of how to install it. Given it was an easy installation, I didn’t need to spend extra for a contractor.

A renter just informed me that a section of a fence came down between my property and the neighbor’s property. I need to figure out who the fence belongs to and, if it is mine, get a contractor in there to fix it.

With each step closer to financial independence, I have less desire to spend time addressing issues with my rentals.

Reason #2: The More Rentals, The More Renter Issues

Not only are there more headaches when it comes to having more rentals, there are more renter related issues as well.

Renter related issues have less to do with the rental unit itself, but more to do with the actual people renting the unit.

I’ve had to deal with lateness in rent payment and the numerous excuses why rent payments were late. The pandemic has created even a more challenging environment for my renters to pay their rent on time.

In addition, I have a couple of renters who are basically non-responsive at this point and have been delinquent on rent for 5 months. They know that the eviction courts have been closed and are clearly taking advantage of the situation.

Additionally, I’ve had to, at times, serve in a psychologist role by listening to renter complaints or issues with other renters and playing mediator as well.

When renters move out of a unit, I need to also deal with some of the messes they leave behind such as an unclean unit or a massive amount of trash left in my front yard.

Once again, as I get closer and closer to FI, my desire to deal with renter issues has greatly diminished.

Reason #3: I Have Concern For New York City As A Good Location For Real Estate Investment

In my opinion, New York City is the best city in the world. Actually, it isn’t just my opinion alone. There are rankings in which NYC is ranked the best global city such as the 2019 A.T. Kearney Global Cities Index.

As a native New Yorker, I believe strongly in the future of the city. But there have been recent events which do turn some heads for me.

Most of my rental properties are located in NYC. There are a few things that are concerning for me as a landlord.

The first is the policy shift to a more renter friendly environment and a more adverse one for landlords. Those policy shifts are detrimental to people looking to rent out properties in NYC which include limiting the security deposit that can be collected to the onerous eviction rules in place.

Second is the tax heavy policy NYC has in place. New York State also has the top ranking of all 50 states when it comes to the highest state and local taxes paid as a percentage of income.

New York is constantly looking to increase taxes. The State recently increased the mansion tax and other real estate transaction taxes in 2019.

They are currently contemplating another millionaire tax to make up for a budget shortfall. 1% of the population pays 50% of the taxes and that 1% is more mobile than ever. What would happen if a few billionaires leave the city? The State would probably try to increase taxes more to make up for the further shortfall, thus driving even more wealthy individuals away. This can lead to a death spiral over time.

Lastly, the pandemic has shown companies that people can work remotely. The financial services industry employees contribute around 20% to the revenue of New York. With remote working, people’s place of residency becomes more flexible. And financial services firms are finding out that they can still run their businesses with employees scattered across geographies.

What will happen to the businesses and the State when people decide to not return back to NYC because they can live in Florida but still work for a Wall Street firm?

Reason #4: I Want Assets That Are Mobile

This pandemic has shown me the benefits to being mobile. I want to have the option to be able to pick up and leave instantly.

In turn, I want assets that can also be mobile and can easily travel with me.

Stocks and cash travel well. I can access my stock portfolio anywhere in the world as long as I have internet access. I can do the same with cash in my bank account as long as I can find a bank.

Real estate is obviously not mobile. If I decide to pick up my life and family and move to another state or country in a short period of time, I would need to leave my real estate portfolio behind.

Since I already have an 8-figure real estate portfolio, do I want to add more to an asset class which isn’t mobile in nature, especially in an increasingly global and mobile world?

Reason #5: Real Estate Has Huge Transaction Costs For Buying And Selling

There are just a huge amount of transaction costs in acquiring and then selling a real estate property.

The biggest of which is realtor fee. In New York City, the typical realtor fee is 6% of the sale price paid by the seller, although that can be negotiated down. The realtor fee takes a big cut out of the proceeds.

There are other costs in addition to realtor fee in NYC. Mansion tax is paid by the buyer on a real estate purchase of $1 million or more. The mansion tax can range from 1% of purchase price to 3.9% on a $25 million purchase. The tiered rate was passed in 2019 from just a flat 1% mansion tax on properties over $1 million.

Title insurance, mortgage recording tax, and transfer tax are some additional transaction costs that add a few percentage points to real estate transactions.

It is costly to buy and sell real estate, especially in NYC. I struggle to think of another asset class with such huge transaction costs.

Reason #6: Even Though Mortgage Rates Are Low, Financing Takes Too Long And Is A Cumbersome Process

Anyone who has recently taken out a mortgage knows that the mortgage application process is a long and cumbersome process. Not to mention, it can be costly too with application fees and appraisal fees thrown in.

Lenders go through a checklist of items to review and request. Some underwriters can be very firm in their review and ask for the world in financial information.

I’ve gone through more mortgage application processes than I would care to admit between financing new purchases and re-financing existing mortgages. Although I have been successful every time, they have never been fun.

I equate getting a mortgage to a financial colonoscopy. Who wants to constantly deal with such a painful process? That is definitely a turn-off on buying more rental properties.

Reason #7: I Already Have Sufficient Real Estate Exposure

After examining my investment portfolio, I feel comfortable with the level of real estate exposure I have. Real estate is a significant part of my overall investment portfolio.

Can I have more? Sure, but I don’t feel the urge to continue to add to my real estate portfolio aggressively like before when I was starting out building my rental portfolio.

My real estate portfolio is already 8 figures in value and heavily concentrated in New York City. My real estate holdings have done well for me for many years.

But I feel that I already have sufficient real estate exposure and adding more isn’t necessary.

Reason #8: My Desire For Passive Income Cash Flow Decreased After Wanting To Work Longer

I’ve listed a number of benefits of owning real estate earlier in this post.

One of the benefits I highly value is the relatively stable cash flow residential rental properties provide. It is important to have a nice passive (or semi-passive) cash flow stream if one hopes to achieve financial independence and to one day walk away from a corporate job.

I was also someone who had a strong desire to be FI and to be free from my corporate job. But the ironic thing is that the closer I get to financial independence, the less I want to leave my job. I have 10 reasons why this is the case.

My desire to leave the workplace is highly dampened, at least in the near term. That makes the need for a steady cash flow stream less important.

I already have a healthy rental cash flow stream. I was hoping to add to it and pad it before I walk away from my corporate job. Now, I can see myself working for a few more years, even for the next decade.

I don’t need to pump up my passive cash flow stream as much anymore. I can invest for appreciation alone. That decreases my demand for real estate.

So Is This The End For Your Real Estate Investing Life?

I don’t believe this will be the end of my real estate investing life. It would probably just be different going forward.

I plan to allocate more of my money in different investments and asset classes. The goal for me now is to look for investment opportunities which are more passive and less hassle than direct real estate investing.

Therefore, a larger allocation will go into other investment types than previously. This will leave a smaller capital allocation for real estate investments. Obviously, by allocating less capital to real estate, I will slow down my acquisition of direct real estate investments.

I plan to be even more selective with my real estate investments in the future and pull the trigger on great deals only. I plan to increase my return target for future real estate investments.

I can also see myself doing 1031 exchanges by selling existing properties I have and rolling the gains into another property. This can be because of a better investment deal or financing terms, a different location exposure or to acquire a higher priced property.

Ultimately, I don’t see myself getting back into heavy rental property purchases until I’ve learned how to scale this investment class. By this I mean I can put a great amount of money to work but that my actual time involvement decreases.

The next step in order to scale is probably acquiring apartment buildings in other states.

Until I can learn to scale my investment in this asset class, my love affair with real estate has definitely waned. Hopefully, I can rekindle the fire sometime in the future.

To the audience: What is your opinion of direct holding of residential rental properties? Have your opinions changed due to the pandemic? Do you have any real estate exposure in your investment portfolio? If yes, what type of real estate exposure is it?

Related Posts – Real Estate Topics

6 Steps To A 10% Cash On Cash Return And 18% Total Return

5 Ways To Acquire Real Estate For Less Than Market Value

How To Maximize Rent And Other Considerations For A Vacant Rental Unit

Hidden Expenses To Owning Real Estate

How One Person Built A Real Estate Empire With Little Money To Start

The Risks Of Buying Rental Real Estate Properties In NYC During The Pandemic

Real Estate Should be Cornerstone of Your Investment Portfolio

$400,000 Income, No Taxes Paid

Many people work hard to better their physical and mental health. What about their financial health?

I started this blog back in 2019 to help people better their financial health as well.

My financial journey began with tens of thousands in student loan debt. Over the span of 20 years, I am close to achieving financial independence.

I truly believe anyone can get to strong financial health. Hopefully, this blog can help you on your financial journey to greater wealth and financial independence.

You can read more about me here.

Thank you for visiting. Come again soon!

I’m actually just contemplating if it’s time I start diversifying a bit into real estate 🙂 My main concern at this point is having an asset which is cemented (literally) into a single location.

Some questions I have from reading your post:

1. Would seem that you could just take a management company to deal with all these units. Isn’t that worth it for you?

2. Have you thought at any point about diversifying your real estate portfolio internationally? Or even to other states?

Cheers!

I am still a fan of real estate, especially for people with limited to no exposure. The trillions of dollars injected by the Fed/US government have to eventually lift real estate prices and the mortgage rates are so attractive right now. The reasons I gave about pulling back are really for my own personal situation.

To answer your questions:

(1) My 20+ units are spread across a number of 2 to 3 family houses. Given the small number of units in each property, a property management company will probably charge me 8% to 10% of gross rent. That isn’t the end of the world for me but it does change the return profile of my real estate investments. I’ll probably take another look at using a management company in the future.

(2) I don’t plan to diversify my holdings to another country. Peter Lynch said to invest in what you know. I feel the same way about real estate. If I am not there or know the area like the back of my hand, I would not feel comfortable investing. My goal is to eventually head south and buy real estate properties in other states. Prices are cheaper down south. I might be able to pick up 30 unit buildings with a dedicated super. That is how I plan to scale my real estate portfolio in the future.

If you want to see how real estate can become a disaster have a look at South Africa. Due to what politicians decide renters cannot be evicted without suitable accommodation, and because there are so many poor, there has been talk of expropriation without compensation. That coupled with huge increases in municipal costs (15% pa over 10 years), corrupt/weak infrastructure and funds being diverted to poorer parts of the city, it is no wonder that capital appreciation in real terms has been negative for years.

As a personal example, we purchased an apartment in the best part of the economic hub of the country for $200k. Although it increased in local currency, due to the weakening of the Rand, that property is now worth $80k 10 years later. At least in usd terms our costs have also dropped, but wanted to illustrate that property can be a poor investment if economic factors are against the investor. This was before the pandemic, so I suspect at present most property is unsellable, so liquidity is key.

Thankfully I’ve never been a big property person so it’s a minor hit to the portfolio, but not all property appreciates in value, and can go backwards in capital value if the resulting municipal costs/taxes exceed inflation over a period of time.

My friend, you are scaring me about what a downside case might be for NYC real estate.

I wouldn’t worry too much unless the last bastion of capitalism gets converted to socialism. If that happens then the whole world is in trouble and it won’t matter anyway.

These things take time, are generally political, so you can see them coming for some time (ref Germany, Zimbabwe, Venezuela, Argentina, etc). Despite its issues the US/NY seems fine unless it loses its reserve currency status.

I live in another part of the world, recently bought an apartment in order to rent it out. This is a great passive income for me. Well, I think it’s all individual. There are many different reasons why this may not work for you.

Yes, investing is very personal. Hopefully your rental is working out well for you and you want to add to your rental portfolio.

Thanks for all these insights.

What key parameters do you look at when investing in real estate – yield?

Do you need to use a lawyer sometimes when dealing with tenants?

Thanks,

A couple of items since I am most interested in have a steady cashflow in this stage of my financial life: (1) I want convenience so proximity is huge for me. If I have to stop by one of my rental properties, it will be less than a 1 hour drive to get there; (2) a cash on cash return that meets my investment criteria.